A private equity partner is answering late-night emails from a home office, hiding withdrawal symptoms behind calendar discipline. A founder's spouse is searching treatment options on a second laptop because the family can't risk the wrong admission call going through a company line. A senior executive knows help is overdue, but the questions pile up fast. Will insurance cover any of this. Will residential care be approved. Will treatment interrupt work, reputation, or both.

For high-achieving professionals, a significant obstacle usually isn't recognizing the problem. It's finding a form of care that matches the complexity of the life already built around them. Insurance coverage for addiction treatment matters in that decision, but so do privacy, clinical depth, room to stabilize, and the ability to stay appropriately connected to urgent responsibilities.

That's why the right residential program isn't a retreat from real life. It's a structured way to protect health, judgment, family stability, and long-term professional capacity while reducing chaos around the admission process.

The Executive's Dilemma Recognizing the Need for Premier Care

An executive rarely presents with a simple addiction story. The alcohol use may be tied to relentless travel, performance pressure, insomnia, or unmanaged anxiety. Prescription misuse may sit beside burnout, trauma, or depression. Cocaine or stimulant use may be hidden inside a culture that rewards output and punishes pause.

The family often sees the consequences before the executive does. Missed emotional presence. Erratic sleep. More defensiveness. More secrecy. More dependence on routines that no longer look optional.

For this population, treatment selection has to solve several problems at once. Clinical care has to be strong enough for dual diagnosis needs. The setting has to be discreet. The environment has to feel safe, not institutional. And the program has to recognize that some residents still need limited, appropriate access to communication while they stabilize. That's one reason families often compare inpatient vs outpatient rehab carefully before making a decision.

What usually doesn't work

Sending a high-functioning professional to the cheapest available option often creates friction from day one. Shared rooms, chaotic environments, weak psychiatric oversight, or rigid communication rules can push the client into resistance before meaningful treatment starts.

A purely outpatient approach can fail for the opposite reason. It may preserve convenience while leaving the person inside the same triggers, access, patterns, and obligations that have kept the addiction in place.

A treatment plan that looks affordable on paper can become expensive if it's the wrong level of care and leads to relapse, early discharge, or repeated admissions.

What families are really buying

In luxury residential treatment, the private-pay portion usually isn't just about appearance. It often secures the conditions that make an executive more willing to stay, engage fully, and complete care. Private rooms matter. Calm surroundings matter. A highly skilled clinical team matters. So does a structure that protects confidentiality while allowing carefully managed continuity with important personal or professional obligations.

That framing changes the insurance conversation. The goal usually isn't to force an insurer to pay for every feature of a premium program. The goal is to use available benefits intelligently so the clinical portion of care is offset, while the family invests in the environment and discretion they want.

Understanding Your Legal Rights for Coverage

Most families start the insurance process assuming the insurer has complete control. Legally, that isn't the right starting point. Federal rules give people seeking addiction care meaningful protections, especially around parity and essential benefits.

What the ACA changed

Under U.S. marketplace rules, mental health and substance use disorder services are an essential health benefit, and plans must cover behavioral health treatment, inpatient mental or behavioral health services, and substance use disorder treatment. Parity rules also prohibit stricter financial, treatment, or care-management limits than those applied to medical or surgical care, as outlined by mental health and substance use coverage rules on Healthcare.gov.

That doesn't mean every plan pays for every facility or every level of care without friction. It does mean addiction treatment is not supposed to be treated as an optional extra in the categories covered by those rules.

What parity means in plain language

Parity is where many families find an advantage. If an insurer uses deductibles, copays, prior authorization, visit limits, or other management tools, it can still do that. What it can't do is impose harsher standards on addiction treatment than it uses for comparable medical or surgical care.

That distinction matters. A family may hear, “Residential treatment requires review,” and assume that's the end of the issue. It may not be. The right follow-up is whether the insurer is applying a comparable standard consistently, and whether the clinical facts support the requested level of care.

Practical rule: Don't ask only, “Is rehab covered?” Ask, “How does this plan apply medical necessity, prior authorization, and reimbursement rules for substance use treatment compared with medical care?”

Why these rights matter for affluent families

High-net-worth families often assume legal protections are less relevant because they can private pay if necessary. In practice, rights still matter because they shape negotiation. They affect reimbursement, appeal posture, authorization strategy, and the strength of an out-of-network claim.

They also matter because the gap between “covered in theory” and “usable in practice” is still real. A policy can include behavioral health benefits while making access difficult through network design, utilization management, or narrow interpretation of medical necessity. The family that understands the rules enters every call more prepared and far less dependent on whatever the first representative says.

Decoding Your Policy for Premier Treatment Access

The most important document in this process is not the insurance card. It's the actual structure of the plan. For executives seeking private, high-end residential care, the difference between a PPO and an HMO or EPO often determines whether out-of-network treatment is financially workable.

A major practical problem is that many insured people don't know their own coverage details. Among privately insured adults with drug use disorders, only 62.4% knew whether their plan covered drug use treatment during 2014 to 2018, while 37.6% did not know at all, according to the PLOS One study on treatment coverage awareness.

Why PPO plans matter more in luxury residential care

A PPO usually offers some out-of-network flexibility. That doesn't guarantee favorable reimbursement, but it creates a path. For a luxury residential setting that may not participate in a standard network, that path matters.

An HMO or EPO is usually less flexible. Those plans often depend heavily on in-network providers, referrals, and stricter network boundaries. If the desired program is outside that structure, the family may have far fewer options for reimbursement.

The terms that actually affect the bill

Families don't need to become insurance experts. They do need to understand a few terms well enough to model the likely out-of-pocket exposure.

- Deductible means the amount the member may need to satisfy before certain benefits begin paying.

- Coinsurance refers to the portion of the allowed amount the member may still owe after the deductible is met.

- Out-of-pocket maximum can limit member responsibility for covered services under the plan's rules, though out-of-network structures can be more complicated.

- Allowed amount matters because reimbursement is often based on the insurer's allowable rate, not the provider's full private fee.

- Out-of-network benefits determine whether any portion of a private residential stay can be offset.

PPO vs HMO or EPO Plans for Executive Rehab Access

| Feature | PPO (Preferred Provider Organization) | HMO/EPO (Health Maintenance/Exclusive Provider Organization) |

|---|---|---|

| Out-of-network access | Often available in some form | Often limited or unavailable |

| Referral requirements | Usually more flexible | Often more structured |

| Fit for private residential treatment | Better suited when the facility is outside the insurer's network | Often harder to use for non-network luxury care |

| Reimbursement path | May allow partial reimbursement for covered clinical services | May offer little or no reimbursement outside network rules |

| Family strategy | Model benefits carefully and verify each level of care | Confirm network restrictions early before pursuing admission |

For high-end treatment, a PPO doesn't make the stay free. It makes the financing strategy more realistic.

What a careful review should answer

Before admission, the family should know whether the plan recognizes detox separately from residential treatment, whether out-of-network behavioral health claims are reimbursable, and how the plan defines medical necessity for substance use treatment.

Many executive families benefit from slowing down. Speed matters in admissions, but rushed assumptions are costly. A polished insurance card and a strong income profile don't automatically translate into strong insurance coverage for addiction treatment.

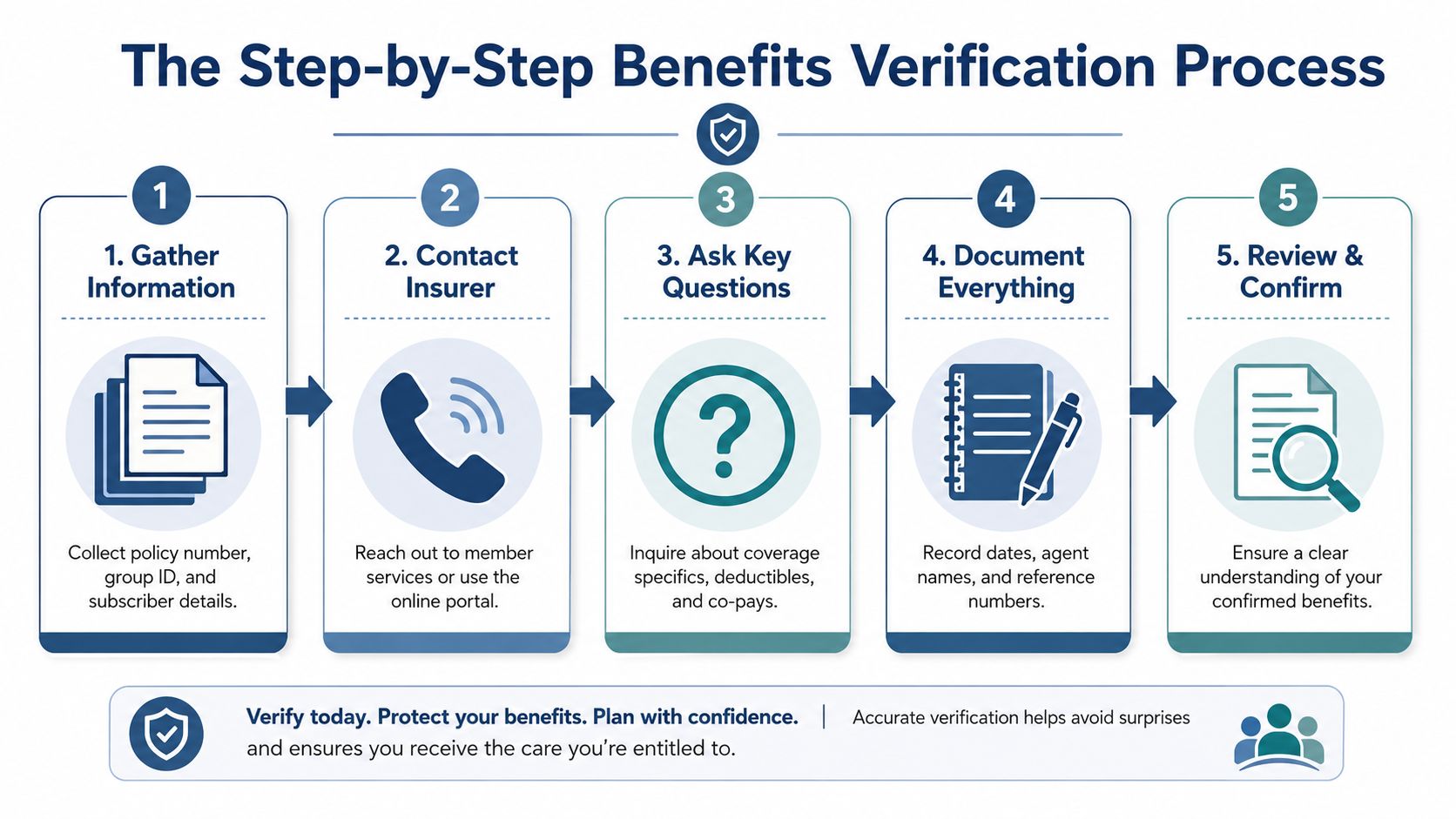

The Step-by-Step Benefits Verification Process

An executive agrees to treatment on Friday afternoon. By evening, the family wants answers on privacy, timing, and cost. The fastest way to lose control of the process is to let insurance questions stay vague.

Benefits verification works best when one person manages it from start to finish. That can be a spouse, general counsel, family office contact, executive assistant, or the admissions team with written permission. Clear ownership prevents conflicting answers, missed authorizations, and expensive assumptions about what a PPO will reimburse.

The five steps that reduce confusion

Collect the policy details

Gather the member ID, group number, subscriber name, date of birth, and the behavioral health phone number on the card if one is listed. If the client has secondary coverage, pull that policy too before anyone calls.Confirm each level of care separately

Ask about detox, medically monitored withdrawal, residential treatment, partial hospitalization, and outpatient follow-up as separate benefit questions. Insurers often review each level of care under different rules, and that distinction affects both approval and reimbursement.Verify the out-of-network payment method

Ask how the plan calculates payment for a non-contracted residential provider. Families should know whether the plan uses an allowed amount, a usual and customary formula, or another reimbursement schedule, and whether a separate out-of-network deductible or coinsurance applies.Document every contact

Keep a written log with dates, call times, representative names, reference numbers, and the exact benefit language quoted. I have seen appeal decisions turn on one call note that confirmed a prior statement from the insurer.Request a treatment-specific verification

General customer service representatives often give broad answers. Admissions staff who work with behavioral health claims every day usually ask better questions about residential eligibility, prior authorization, and claim submission. Families comparing private options can review this explanation of private rehab covered by insurance before making financial decisions.

The questions worth asking verbatim

A short script keeps the call focused and reduces room for vague answers.

Level of care question

“Does this plan provide benefits for detox and residential substance use disorder treatment, and are those benefits reviewed separately?”Out-of-network question

“What out-of-network benefits apply to behavioral health or substance use disorder treatment at a non-contracted residential facility?”Authorization question

“Is prior authorization required before admission, who is allowed to request it, and what clinical records are needed?”Cost-share question

“What deductible, coinsurance, and member responsibility apply to covered out-of-network behavioral health treatment?”Claims question

“Are claims paid directly to the facility, to the member, or both, and what claim form should be used?”Documentation question

“Please give me a reference number for this call and note the benefits we discussed.”

If the policy also includes outpatient mental health coverage, it helps to verify therapy benefits for 2026 while the insurer is already on the line. That matters for discharge planning and for executives who expect to continue treatment while returning to work.

Prior authorization deserves close attention

Prior authorization can shape the entire financial outcome of a private admission. If the clinical picture is presented incompletely, the insurer may approve fewer days, approve a lower level of care, or delay the review long enough to create pressure around admission timing.

The strongest authorization requests are organized, clinical, and specific. They usually include withdrawal risk, current substance use pattern, psychiatric symptoms, relapse history, prior treatment episodes, medication issues, and any safety concerns affecting the ability to remain at home or continue working. For executives and public-facing clients, speed matters, but accuracy matters more. A rushed submission can cost far more than the time saved.

Families should also ask one practical question early: who will coordinate updates once the client is admitted? Ongoing reviews often determine whether continued stay days are approved. When that responsibility is assigned clearly, the family gets better visibility into expected reimbursement and a more realistic estimate of the out-of-pocket investment tied to privacy, comfort, continuity, and clinical intensity.

What Insurance Actually Covers in Luxury Rehab

Expectations must be precise: insurance usually pays for covered clinical care, not for every feature that makes a premier residential program appealing to executives and families.

That difference isn't a flaw in the process. It's how premium treatment financing works.

What the plan is more likely to recognize

When a stay is reimbursable, the insurer usually focuses on the clinical components tied to diagnosis, stabilization, and treatment. That can include psychiatric evaluation, medication management, physician oversight where applicable, individual therapy, group therapy, and treatment planning if those services meet the plan's coverage rules.

The conflict often appears at the level of care stage. Coverage for addiction treatment is not always all-or-nothing. A review cited in the peer-reviewed literature found that 21 states did not cover residential treatment and 9 states did not cover intensive outpatient services, showing how benefit design can exclude certain settings even when behavioral health coverage exists, as discussed in this review of insurance benefit design and substance use treatment access.

What the private-pay portion usually secures

Luxury residential treatment includes value that an insurer typically doesn't underwrite in full. For executive and high-profile clients, that often includes:

- Private accommodations that reduce overstimulation and support discretion

- Enhanced privacy practices that matter to public-facing professionals and families

- A more contained environment with lower census and more individualized pacing

- Executive-compatible logistics such as appropriate access to electronics when clinically approved

- Wellness-focused and comfort elements that improve willingness to stay engaged in care

Those features may be central to the family's decision, but reimbursement usually follows the clinical side of the stay, not the premium experience itself.

The family is often using insurance to offset medically necessary treatment while privately funding the conditions that make treatment workable for the client.

Why residential requests are often contested

Some insurers accept outpatient treatment more readily than residential care because residential treatment is more intensive and more expensive. That's why strong clinical documentation matters. If the person has withdrawal risk, relapse risk, co-occurring psychiatric needs, poor containment outside a structured setting, or repeated unsuccessful lower levels of care, those facts become central.

Families who want a broader framework for policy interpretation may find it useful to verify therapy benefits for 2026 before they compare residential and outpatient coverage assumptions. It won't answer every residential question, but it helps clarify how behavioral health benefits are often structured.

For a more realistic budgeting discussion, it also helps to review the average cost of addiction treatment alongside likely reimbursement rather than treating insurance as an all-or-nothing yes or no.

Proactive Strategies for Denials and Appeals

A denial is frustrating, but it isn't final. In addiction treatment, many denials reflect disagreement about level of care, network status, or documentation quality rather than a clean statement that no benefit exists.

That distinction matters because appeals succeed or fail on precision.

Why denials happen even when coverage exists

Insurance-related barriers remain substantial. One study found that 39% of low-income adults with a treatment gap cited insurance barriers, with no significant reduction after the ACA, according to this study on treatment gaps and insurance barriers.

In practical terms, denials often turn on one of a few arguments:

Medical necessity challenge

The insurer argues outpatient care is sufficient.Incomplete authorization file

Clinical records don't clearly justify residential structure, detox oversight, or psychiatric complexity.Out-of-network limitation

The plan acknowledges some benefit but narrows reimbursement sharply.Administrative mismatch

Dates, coding, authorization timing, or submission details don't line up.

What improves an appeal

The strongest appeal is usually clinical, organized, and fast. It should explain why the requested level of care is appropriate for this patient now, not in general. Generic statements rarely move the reviewer.

Useful appeal material often includes:

- A clear diagnosis summary with substance use and co-occurring psychiatric concerns.

- Recent risk factors such as relapse pattern, withdrawal concerns, impaired functioning, or safety issues.

- Treatment history showing why a lower level of care may be inadequate.

- Current physician or clinical recommendation tied to the requested level of care.

- A point-by-point response to the insurer's stated reason for denial.

Appeals win more often when the treatment team answers the insurer's exact objection instead of restating that care is important.

Internal appeal and external review

An internal appeal asks the insurer to reconsider its own decision. An external review asks for an independent look after internal options are used or when the policy allows it. Families shouldn't assume the first denial letter explains this clearly. Deadlines matter, and so does the paper trail.

For families who want a practical overview of documentation and timing, these effective strategies for denied claims can help organize the process.

What doesn't work

Anger on the phone rarely changes an adverse determination. Neither does arguing only from status, urgency, or willingness to pay privately. The insurer responds to record support, benefit language, and procedural compliance.

The high-value move is to build a file that is difficult to dismiss. In executive cases, that often means showing not just substance use severity, but the interaction between addiction, psychiatric strain, occupational pressure, sleep disruption, family destabilization, and failed attempts to self-manage outside a structured setting.

Conclusion Investing in Your Career and Your Future

Executives rarely need convincing that delay has a cost. They understand what happens when a manageable problem is left to widen inside a high-consequence role. Addiction works the same way. The cost isn't limited to health. It reaches judgment, credibility, family trust, and long-term capacity.

That's why insurance coverage for addiction treatment should be treated as a financing tool, not the sole decision-maker. Legal protections matter. Policy structure matters. Benefits verification matters. Appeals matter. But the deeper question is whether the setting and clinical model fit the person who needs care.

For a high-net-worth family or working professional, the out-of-pocket portion often purchases things insurance doesn't fully value on a claim form. Privacy. Containment. Clinical sophistication. Private accommodations. A setting where recovery can begin without creating avoidable professional fallout.

There's also a system-level reason to work with treatment programs that understand payer mechanics well. Better documentation, cleaner authorization files, and stronger claim handling reduce friction for everyone involved. For readers interested in the billing side of behavioral health operations, this resource on how providers boost behavioral health revenue offers a useful look at why denials happen and how disciplined processes improve outcomes.

The best insurance strategy is the one that reduces chaos while preserving access to the right level of care. For executives, that isn't indulgence. It's risk management with a human center.

Reflections provides confidential support for professionals and families evaluating luxury dual-diagnosis treatment, including private residential care, sub-acute detox, PPO and out-of-network insurance review, and admissions guidance designed to minimize disruption while protecting privacy. Explore options at Reflections.